Everything you need to know about Payment Aggregators

FinTech, the new-age portmanteau has effectuated a whole slew of new stakeholders in the technology driven finance world- Payment Aggregators, Payment Gateway Providers, Payment Processors, and more. As we extensively use more new innovations making the cashless economy our new digital future, it is important to know how the digital payment portals’ function and the various stakeholders working in tandem to facilitate the payment process.

Although the FinTech is an umbrella term that refers to all financial services powered by technology, we will elaborate on some of the basic terms used in digital payments. You may refer to our FinTech Glossary for a quick learning of the various FinTech jargon. If you are customer scanning a QR (Quick Response) code in a Kirana Store or a small business owner with a QR scan code displayed in your store, or if you are just plain curious, here is a starter pack to understand some basic inner mechanics of the FinTech world.

What is Payment Aggregator?

TThere are several payment modes currently available in the marketplace. For Retail and e-commerce, the offline and online payment modes need to be unified and seamless to provide a smooth payment experience for your customer. The Payment Aggregator integrates several different payment modes and offers the platform for a business (merchant) to use. The business, both retail and e-commerce outlets, can use the payment aggregator platform to collect payments from its customers.

Why are Payment Aggregators called Merchant Aggregators?

Payment Aggregator is also referred to as a Merchant Aggregator because it signs up all merchants directly under its own MID (Merchant Identification Number) to process transaction through a single master account. Payment Aggregator provides the merchant with a sub-merchant account. Merchants are not required to acquire a merchant account from the bank.

Why do businesses need Payment Aggregator?

Today’s marketplace straddles both online and offline space to stay in business and more importantly to stay relevant. The precarious balance between both is undoubtedly a challenge as business decisions, marketing efforts, and overall customer experience needs to be unified, swift, smooth, and accessible.

Payment Aggregator, a technology driven solution offers all-in-one payment solution to the challenges that arise with running a business in a dynamic marketplace. This applies to all businesses irrespective of the location, size, revenue, sector, or industry, etc. Payment Aggregator integrates all payment modes- PoS (Point of Sale) terminal, cash, cheque, and digital payments such as debit or credit cards, internet banking, e-wallets,UPI (Unified Payments Interface), EMI (Equated Monthly Instalment), and more, in both retail & e-commerce space.

What is the function of Payment Aggregator?

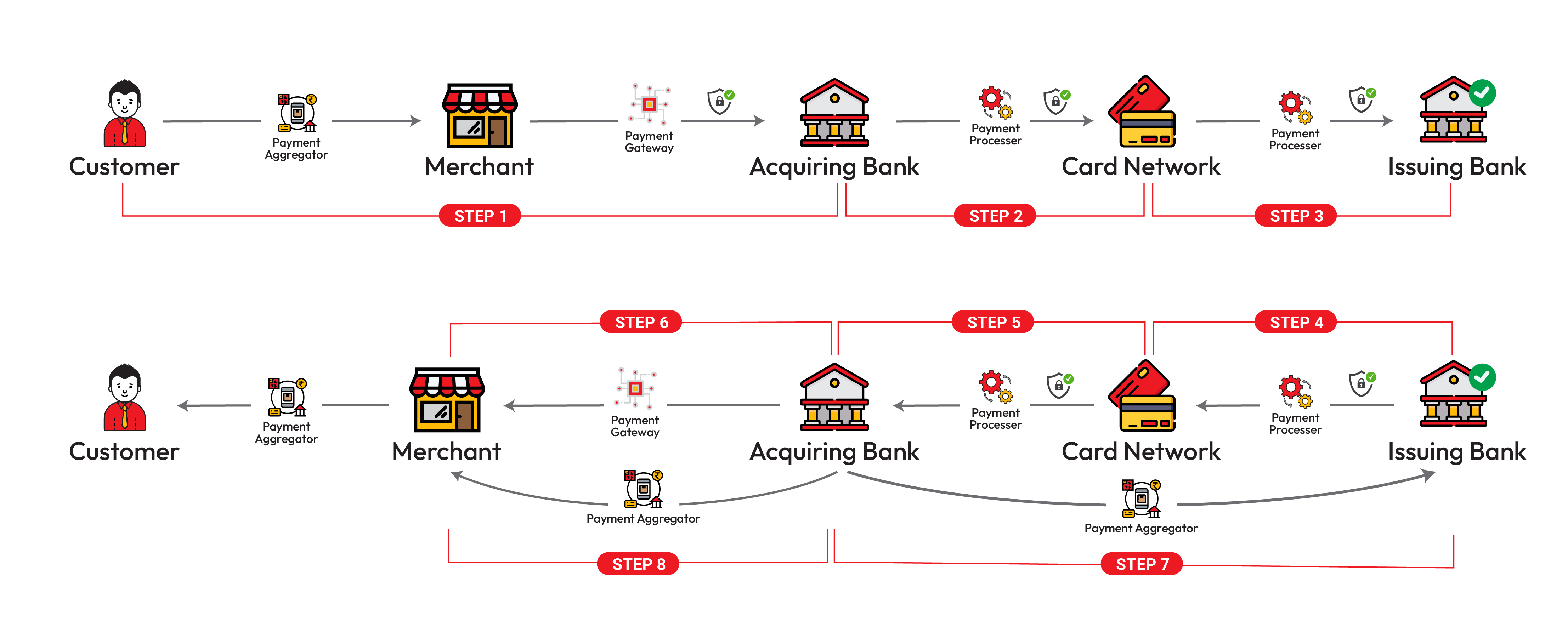

The term Payment Aggregator is often assumed to have the same role and function as a Payment Gateway. Both are two distinct entities that function in tandem to complete the payment process, the difference is explained in the latter part of the blog. Here is a comprehensive step-by-step process of how Payment Aggregator functions.

Step 1: Customer begins the checkout process to purchase a product or service- In a retail outlet or an online e-commerce store. The customer chooses the payment mode (Credit/Debit Card, Internet Banking, UPI, EMI, etc.) and enters the relevant payment details. Payment Gateway encrypts the data and performs a fraud check.

Step 2: The customer’s information is relayed to the acquiring bank. With the help of Payment Processor, the acquiring bank checks and sends the customer information to the corresponding card service provider (Visa, MasterCard, etc.)

Step 3: The Card service provider verifies the customer information and performs a fraud check. Subsequently, the Payment Processor relays the information to the issuing bank

Step 4: The issuing bank verifies the customer’s details and checks for sufficient funds in the account. This triggers a response of approval or denial of the payment and is sent to the card service provider.

Step 5: The Card Service Provider notifies the acquiring bank about the approval or denial of the payment via the Payment Processor.

Step 6: The Payment Gateway relays the status of payment i.e., approval or denial of payment to the merchant from the acquiring bank.

Step 7: If the payment is approved, the acquiring bank of the Payment Aggregator requests the issuing bank to release the funds.

Step 8: Upon receiving the funds, the Payment Aggregator proceeds to settle the funds in the merchant account based on the settlement cycle, which is generally T+2 to 3 business days (T = Day of Payment Capture).

Payment Aggregator, Payment Gateway & Payment Processor

Payment Aggregator, Payment Gateway, and Payment Processor are cogs in the same machine. One cannot function without the other. In simple terms, the three distinct components and their corresponding functions are as follows:

Payment Aggregator unifies several different payment modes and provides it as a service to merchants (businesses) enabling them to accept/collect payments from their customers.

Payment Gateway provides the technology infrastructure to capture and send customer’s payment information to and from the Payment Processor. It also communicates the approval or rejection of the payment to merchant and customer.

Payment Processor safely routes the customer’s data among the different parties i.e., acquiring bank, card service provider, and Issuing bank).

As we gradually traverse into the digital world, it is essential to have a basic understanding of the different components that work seamlessly to provide the improved and efficient payment services. Know more about Pay10 Payment Gateway, Payment Links, Payout services, Billing service, Reseller services, and more.